WHAT WE OFFER

Delcap DBI/RDT Portfolio

Would you like more information ?

About DBI/RDT

Dividend received deduction is a tax exemption regime whereby, under certain conditions, a company can fully deduct the withholding tax paid on dividends it received from another company from its taxable profit.

The underlying reasoning is that the distributing company has already been taxed on its profitability. By exempting the dividend from corporation tax on the level of the receiving company, a double taxation is avoided.

3 conditions must be cumulatively met in order to profit from this exemption :

Holding requirement: The receiving company holds the shares in full ownership for an uninterrupted period of

at least 1 year.

Taxation requirement: The distributing company is subject to corporate income tax, in Belgium or abroad, under a

normal tax regime.

Participation requirement: The receiving company holds at least 10% of the shares of the distributing company or a total invested amount of

at least EUR 2,500,000.

Due to the complexity, it is too difficult for most Belgian companies to comply with all criteria for individual investments.

Fortunately, DBI/RDT funds offer an interesting, more accessible alternative.

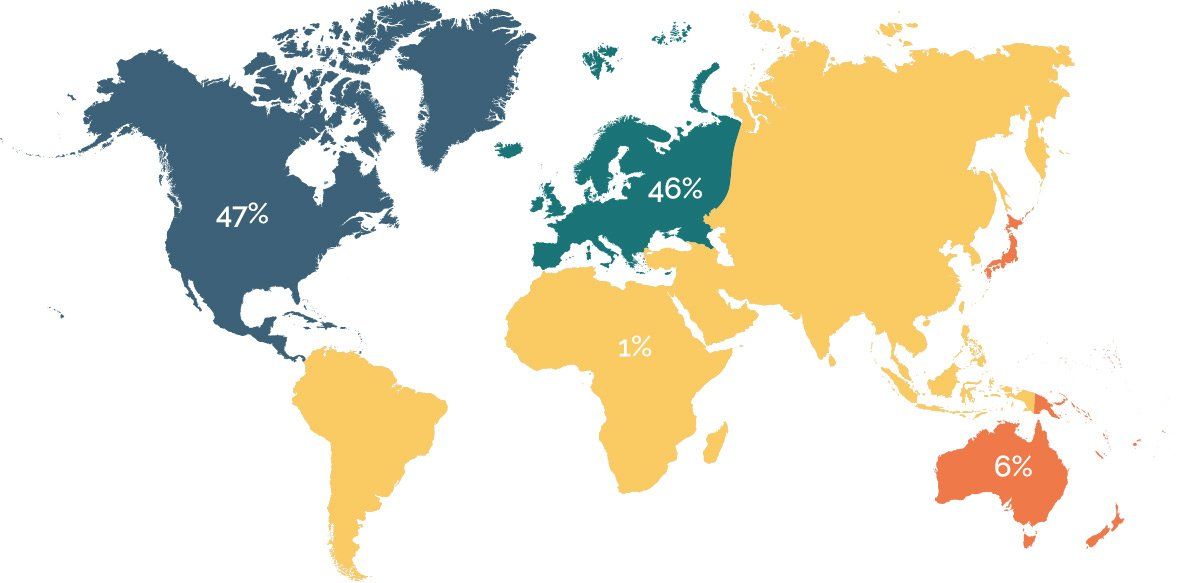

Since 2018 the range of funds on offer on the Belgian market has grown exponentially. Today,

more than 20 managers offer funds with varying strategies, compositions and results.

DISCLAIMER

Past performance is not a reliable indicator of current or future results

Tax treatment depends on the individual circumstances of each investor and may be subject to change. Investors are therefore recommended to seek independent tax advice.